Verification of Payee: A Promising Start

In accordance with Regulation (EU) 2024/886 of March 13, 2024, Payment Service Providers (PSPs) in the Eurozone are now required to offer a beneficiary verification service for both standard and instant European credit transfers. This service, commonly known as VoP (Verification of Payee), has been mandatory since October 9, 2025.

In an op-ed published in La Lettre du Trésorier No. 440 (March), Guillaume Cazenave, Cash Management Expert - Treasury Solutions, and Olivier Hollette, Head of Product Management & Expertise, Natixis Corporate & Investment Banking, share on encouraging early feedback, challenges ahead and development priorities.

Guillaume Cazenave

Olivier Hollette

The process involves comparing the beneficiary's name as registered with their bank against the name provided by the originator. This comparison generates a match status, which the originator can then use to decide whether to approve their payment instruction.

The core challenge of VoP lies in the quality of the parties' identification data - its collection, storage, and transmission. Beneficiary verification begins long before the comparison algorithm is applied. It starts during the initial onboarding phase between all payment participants (banks and clients) and requires ongoing, rigorous updates to third-party data.

The initial observation is that VoP for bulk payment instructions, as submitted by corporates, often in files, has not yet been fully implemented. Therefore, the available figures primarily reflect data from individual consumers and single payments made via banking portals.

The experience of recent weeks shows a relatively neutral impact of VoP on the volume of European credit transfers, both standard and instant.

Positive Early Findings

One of the major concerns surrounding VoP was a potential increase in abandoned transactions, leading to a decrease in European credit transfers (SCT or SEPA Credit Transfers), particularly for individuals. Messages like "This beneficiary does not match; it could be fraud" could understandably cause anxiety among a public not yet fully informed.

The experience of recent weeks shows a relatively neutral impact of VoP on the volume of European credit transfers exchanged, both standard and instant.

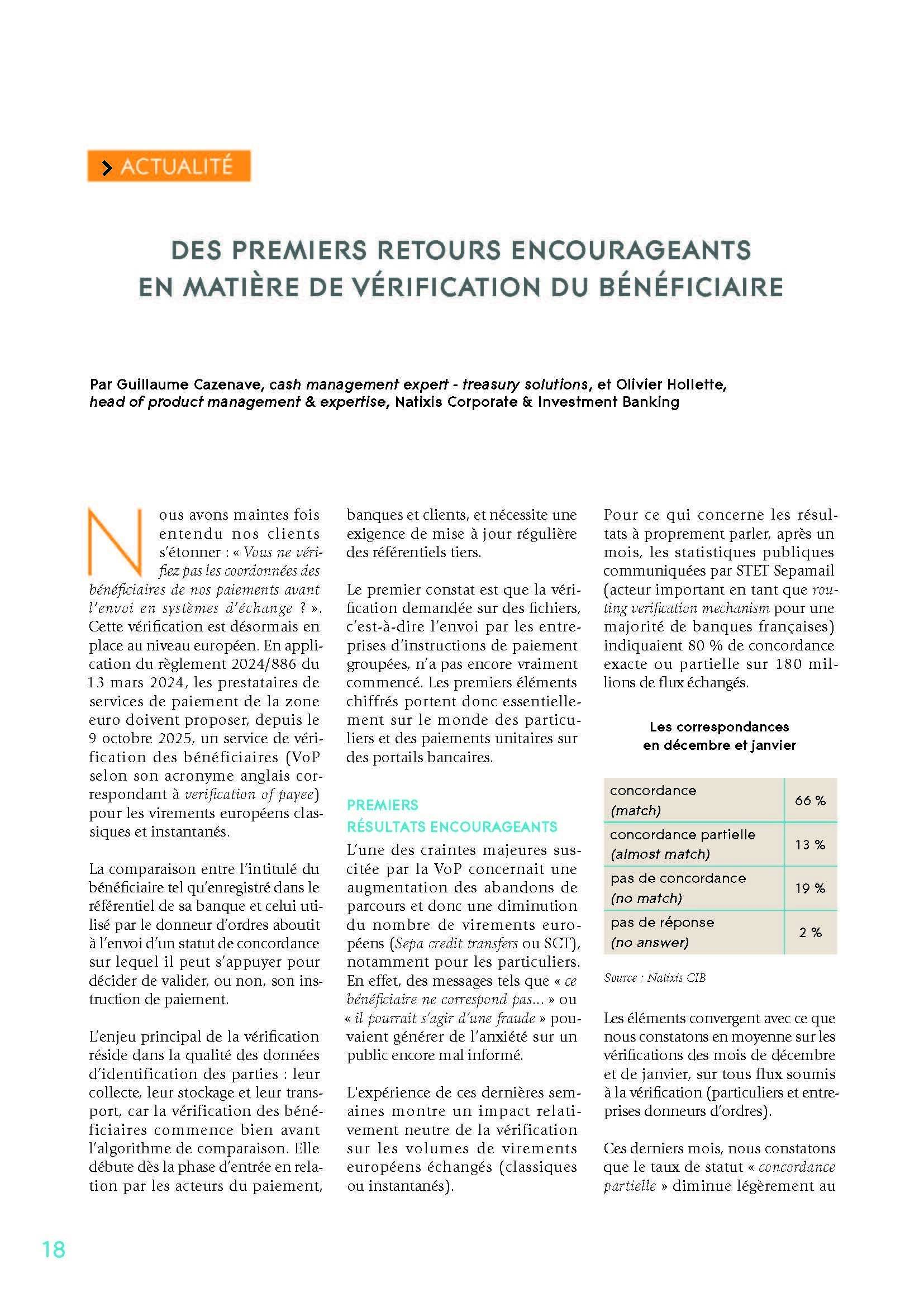

Regarding the VoP results themselves, public statistics released by STET Sepamail (a key Routing Verification Mechanism - RVM - for a majority of French banks) after one month indicated an 80% match or partial match rate across 180 million transactions processed.

December and January

Match Breakdown

MATCH 66%

ALMOST MATCH 13%

NO MATCH 19%

NO ANSWER 2%

These figures align with our general observations for December and January across all transactions subject to VoP, for both individuals and corporate originators.

We have observed a slight decrease in "partial match" statuses in recent months, with a corresponding increase in "exact match." It is important to remember that in cases of a partial match, the payment originator receives the name as held by the beneficiary's account-holding bank. This allows him to make necessary adjustments for future payments.

However, these promising early results also highlight existing challenges and confirm some anticipated concerns.

The Challenge of Bulk Payments

Initially, the focus for Eurozone banks and other PSPs was on complying with the regulation. They proactively communicated about the upcoming legislation, how to prepare, and how to use the new service daily.

The legislator designed VoP as an additional step in payment initiation, introducing a final check before approval and exchange. In the corporate world, payment instructions are often submitted in batches within files, using various transmission and signing methods.

Integrating this extra step across all participants in the payment chain – banks, corporates, and software providers – presents a significant challenge. While some of our corporate clients have already made the transition, the majority are still in an observation and assessment phase.

Questions are arising regarding the best scenarios to adopt, how to effectively utilize the results, the capacity of the VoP system (banks and RVMs) to handle high transaction volumes, and the impact on processing times. As has been the case in recent months, clients are encouraged to engage with their banking partners to discuss these considerations.

The Issue of Repositories

Within the VoP mechanism, banks provide data from their client repositories, including the legal entity name from corporate registration documents. This may also include a commercial name and other identifiers.

The process of invoicing brings up the question of the name a creditor presents to their payer. For instance, we've encountered misunderstandings related to bank account details (RIBs) that sometimes contain an account holder name which may differ from the company's legal name.

Consequently, originators can become confused when they don't achieve a perfect match, even if they've entered a payee name directly from an official bank document. This highlights an issue that previously went rather unnoticed and requires improvement from all stakeholders in the payment ecosystem.

The intra-community VAT number appears to be an excellent candidate for institutionalizing VoP based on identifiers.

Moving Towards Identifier Usage

For corporate entities, a highly effective way to stabilize databases is the use of standardized identifiers, such as VAT numbers or Siren/Siret numbers. These are far less prone to interpretation – if not to say manipulation - than traditional names, making them a stronger defense against fraud.

The intra-community VAT number, particularly relevant with the ongoing e-invoicing initiatives, appears to be an excellent candidate for institutionalizing VoP based on identifiers. To promote their widespread use, we need to address their collection and transmission, while ensuring that account-holding banks declare their availability for querying on these same data points within the EPC Directory Service, the VoP directory maintained by the European Payments Council.

Strengthening Third-Party Data Integrity

VoP results should also be leveraged to enhance the integrity of beneficiary data, directly addressing a critical need in the fight against fraud. Currently, the regulation does not mandate using VoP to verify entire third-party databases outside of the payment initiation process.

However, this is a strong demand from corporate treasurers and accountants. Commercial service offerings are being explored to meet this need.

As the regulation currently stands, VoP implementation allows companies to progressively verify their European payments and, in the background, update beneficiary details.

Another Layer of Security

By Chrystel-Anne Pomel, anti-fraud coordinator

VoP addresses the need for reliable beneficiary data in transfers while maintaining transaction speed (for Instant Payments or SCTs). This is crucial given the prevalence of fraud, often resulting from manipulation of both corporate and individual clients.

However, this solution could create a false sense of security, as it is only one element of transaction safeguarding. Complete protection relies on multiple layers, not a single mechanism.

Fraudsters are constantly adapting and possess a deep understanding of banking processes. They are already finding ways to circumvent this system, for example, by implying that VoP works better for individuals and suggesting that transfers be made out to the company's CFO.

To bolster security, it is imperative to scrutinize data much earlier in the payment execution process, focusing on the quality of the IBAN/account holder pairing (mastering third-party data). Regulatory evolution in this direction for VoP would be a significant advantage.

A Game Changer

Imagine a world where you can be absolutely certain you're paying the correct beneficiary with a single click, regardless of the destination of funds. VoP is an excellent initiative, long-awaited by the entire payment ecosystem, and most importantly, by our clients.

It aligns with recommendations from the FATF and G20 to enhance transparency in capital flows and combat fraud, driven by major international powers aiming to make international transfers faster, more accessible, transparent, secure, and cost-effective.

In their efforts to combat money laundering and terrorist financing, banks adhere to strict, ever-evolving rules. VoP contributes to this by strengthening the use of rich and reliable data.

Concurrently, it is prompting our clients, much like the ongoing ISO migration, to embrace the new reality of collecting and transmitting richer information in a more structured manner within their payment files.

See original in French