The ECB will set things in motion next month

Bringing us Natixis CIB’s views on the hot topics of the moment, Dirk Schumacher, Head of European Macro Research; Théophile Legrand, European Rate Strategist, and; Nordine Naam, Forex Strategist, share the outlook for the weeks ahead.

Eurozone Economy Overview – Dirk Schumacher

The euro area started to show growth again at the beginning of 2024, after 5 quarters of stagnation. In Q1, we had growth of 0.3%qoq, which we expect to continue more or less at that pace – an annualized rate of more than 1%. Although not great, but still decent given many of the structural headwinds the euro zone has faced, it does signal a genuine recovery. From a cyclical perspective there will not be much inflationary pressure despite the growth we are seeing.

Growth in Q1 appears to be supported by monthly indicators (e.g. Euro area PMI - April). That said, there is a significant dichotomy between services – which are performing well – and the manufacturing sector – which, although is not as depressed as it was 12 months ago, is still at a fairly low-level despite the recent rebound in activity.

In terms of fiscal policy, we have seen significant differences in deficits (Italy at more than -7% in 2023, France at more than -5%, and Germany & Spain at close to -2%), which means the growth we have seen in Italy has, to a certain extent, been driven by expansionary fiscal policy. Going forward, the deficit is too high and cannot continue in this direction - the question for the ECB then, is how much fiscal tightening will we see? And for 2024, the ECB has forecasted a positive change in fiscal stance – meaning that we should a small decline in growth on the back of fiscal consolidation. That said, there remains a lot of uncertainty as we don’t know how much consolidation we can expect to see, and this is further complicated by new Euro area fiscal rules.

Dirk Schumacher

Going forward, the deficit is too high - the question for the ECB, is how much fiscal tightening will we see?

Turning to inflation, in principle, things are moving in the right direction. Headline inflation stood at 2.4% in April. Goods price inflation has dropped, indicating that supply shocks had driven good prices up, and as the shocks have been resolved, inflation has unwound. Services inflation has declined to 3.7% after holding steady at 4% for five months. A moderation of wage growth is needed to cool service price inflation to a more comfortable level. Current country data for Q1 paints quite a mixed picture.

June inflation projections are unlikely to show significant change in the inflation outlook, justifying (in principle) a steady decline. Our baseline remains a steady decline at each meeting – subject to wage data and statements from the ECB.

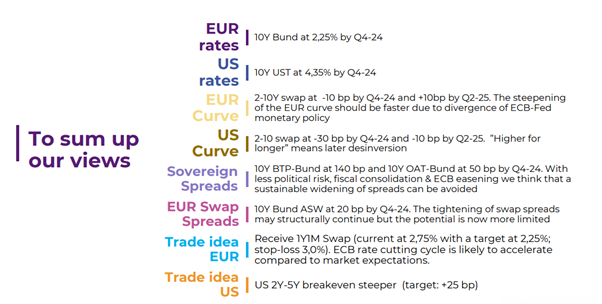

Rates Outlook – Théophile Legrand

The developed rates market has been sensitive to upward surprise in the US economy and inflation, which has led to a repricing of rate cut expectations. The spillover effect on Euro rates is strong. Since early January the market has removed almost 100bps for the ECB and 120bps for the Fed. While this may be justified in the US as disinflation proving to be much slower than expected, in the Eurozone, there is increasing indication that inflation is heading towards the 2% target – thus starting the rate cutting cycle in June and continuing – signaling that the market is underestimating ECB capacity to be independent from the Fed.

Looking at rates market, we saw an acceleration in the rebound of US treasury yields which came to a halt in recent weeks, for two reasons: at the last FOMC meeting, a rate hike this year was ruled out and secondly, April inflation slowed more than expected. Thus, we maintain our view that current Eurozone rates pricing does not reflect economic fundamentals. Decorrelation has already started, and we expect this decorrelation between Euro and US rates to be reinforced in the coming months. Our current US rates scenario forecasts just under 2 cuts of 25bps, with the first rate cut – if it is to happen – taking place in September or November this year.

Our current US rates scenario forecasts 2 cuts of 25bps, with the first rate cut – if it is to happen – taking place in September this year

Théophile Legrand

Moving to EUR sovereign spreads, we continue to see high risk appetite and as a result, continued (but limited) tightening. Looking through the rest of the year, we expect to see a tactical widening of sovereign spreads over the summer, but we believe the structural stability we see at present may persist .

FX Outlook – Nordine Naam

Starting with the USD, the dollar remains strong. It is testing a high level. It has rebounded quite a lot since the beginning of the year, in line with the depricing of the Fed. While most currencies have declined against the dollar, the Euro has managed to resist, and Sterling has been the outperformer so far this year. Swiss Francs and the Yen, which have lowest interest rates, are the underperformers.

The big question now is what’s going to happen next?

In the short term, the Fed’s higher for longer is good for the dollar. In our view, we don’t expect a big decline in USD rates by end of the year, the dollar should be quite stable, but could decline if we see further inflation deceleration – and therefore further rate cuts expectations – but that’s not the case at the moment.

Nordine Naam

In the short term, the Fed’s higher for longer is good for the dollar. As we don’t expect a big decline in USD rates by end of the year, the dollar should then be quite stable.

The EUR/USD has remained quite tightly correlated with the 2 year spread between the US and the eurozone since the beginning of 2023. This is largely related to ECB and Fed policy, but also the positing of the market. Should the ECB decide to cut more than expected, it could lead to a weaker Euro over the summer, but that is not the case for the time being.

Looking at the USD/JPY, the yen has weakened considerably since 2023, reaching historically low levels against the dollar.

The relationship between the USD/JPY and the US/Japan long-rate differential is strong, as it reflects the monetary policy expectations of the Fed and BOJ. Reduced expectations of a Fed rate cuts have contributed to the increase in US long rates, while the BOJ's persistently dovish stance has limited the rise in Japanese long rates. However, Japanese long-term rates have recently increased due to the prospect of the BOJ reducing its purchases of JGBs to counter the yen's depreciation. Nonetheless, the USD/JPY should be lower, given the US/Japan yield spread. Based on our model, which considers the spread of US/Japan long-term rates and the 3-month implied volatility, it suggests to us that the theoretical value of the USD/JPY should be approximately148 as of today.

Taking a look at the USD/CNH, we expect to see a decline to 7.15 by the end of the year, based on a weaker dollar and US bond yields and stronger China growth as signaled by slightly improved PMI data.

To find out more: