Electricity: A Pillar of European Reindustrialization?

The last two decades have demonstrated that electricity costs have played a crucial role in the European Union's slower progress compared to China and the United States, particularly in high-volume industries like aluminum and steel. This has also led to a broader decrease in the manufacturing sector's contribution to the GDP of Europe.

Ivan Pavlovic, Senior Energy & Hybrids Specialist, Hadrien Camatte, Senior Economist, Euro zone, and Bernard Dahdah, Senior Commodities Analyst, explore the intricate relationship between electricity prices and industrial competitiveness in the EU.

Ivan Pavlovic

Hadrien Camatte

Bernard Dahdah

Electricity and Industrial Competitiveness

Electricity is a cornerstone of industrial competitiveness, affecting operating costs, investment decisions, and the carbon footprint of products. In energy-intensive sectors such as aluminium production, electricity can constitute up to 40% of operating costs – a not insignificant amount!

Thus, stability and predictability in electricity pricing are crucial for fostering a competitive industrial environment. When electricity prices are volatile or excessively high, industries may struggle to maintain their competitive edge, leading to reduced production, investment hesitance, and potential relocation to regions with more favorable energy costs. Added to this, the carbon footprint associated with finished products now also plays a role in decisions – notably the EU aims to reduce greenhouse gas emissions by at least 55%[1] by 2030.

When electricity prices are volatile or excessively high, industries may struggle to maintain their competitive edge, leading to reduced production, investment hesitance, and potential relocation to regions with more favorable energy costs.

The energy crisis in 2022 highlighted long-standing trends affecting European industry, particularly the EU's declining competitiveness compared to China and the United States since the early 2000s. The crisis exacerbated an existing cost-competitiveness deficit, especially in high-volume sectors like steel and aluminum, due to significant differences in electricity prices, keeping in mind that EU steel producers have been also penalised by high labour costs and rising carbon constraint.

Although early 2024 saw a slight decrease in EU electricity prices, the gap with the U.S. and China remains significant, exceeding 100% and indicating a continued challenge for European industry in maintaining competitiveness on the global stage.

Production Constraints

Fuel costs, Carbon costs, network charges and end customer taxes all contribute to the price differentials seen across markets, but gathering comparative data on these elements across the EU, China, and the US is challenging.

One factor significantly impacting electricity production in the EU, is the constraint on carbon emissions.

Carbon pricing mechanisms in the EU, China, and the U.S. differ greatly in maturity, impacting overall electricity prices and international price differentials.

The EU has implemented a robust Emissions Trading Scheme (ETS) since 2005, which has recently been reinforced as part of the EC’s Fit for 55 climate package. This cap-and-trade system covers electricity and heat generation, alongside other sectors (heavy industries and aviation), requiring power producers to purchase CO2 emission allowances through auctions or in the secondary market to cover their actual emissions.

The cost of these allowances directly affects wholesale electricity prices. For instance, holding all else equal, a €50/tCO2 EU allowance price can add approximately €20/MWh for gas-fired plants and €42.5/MWh for coal-fired plants. The price of EU allowances has risen dramatically, from under €10/tCO2 to over €100/tCO2 since 2017, leading to the closure of several coal-fired plants in the EU between 2018 and 2021.

In contrast, China's ETS, introduced in 2021, is less developed and covers coal and gas-fired plants in a lenient, benchmark-based approach, resulting in low allowance prices. The U.S. lacks a nationwide ETS, relying instead on regional initiatives, with California leading the way since 2012 with a more advanced carbon pricing mechanism that has seen higher allowance prices compared to other regions.

Accounting Standards and Market Dynamics

The influence of accounting standards on the development of power purchase agreements (PPAs) is significant on both sides of the Atlantic. Industrial customers often opt for bilateral PPAs to secure long-term electricity costs, particularly in the renewable energy sector, which has seen substantial growth over the last 15 years. These agreements allow customers to stabilize their electricity costs, especially as renewable energy sources have become increasingly competitive due to a remarkable decline in generation costs.

However, industrial customers face challenges in ensuring a stable electricity supply, often requiring additional agreements with electricity suppliers to complement their PPAs. They tend to prefer virtual PPAs over physical ones due to the complexities involved in connecting new renewable capacity to existing sites.

The difference in accounting treatment between Europe and the U.S. has likely played a significant role in the adoption of virtual PPAs. Under International Financial Reporting Standards (IFRS), European companies must classify virtual PPAs as derivative financial instruments, which can introduce significant income statement volatility. In contrast, U.S. GAAP allows for more favorable accounting treatment, classifying them as executory contracts without mark-to-market requirements. This disparity has historically hindered European companies from entering into PPAs, impacting the overall pace of PPA development.

Post-Pandemic Challenges in Eurozone Industrial Production

Following the Covid-19 pandemic, industrial production in the Eurozone initially showed resilience, recovering to pre-crisis levels by December 2020 after a sharp decline during the lockdowns. However, recovery was uneven across the Eurozone's leading economies. Italy and Spain returned to pre-crisis production levels by the end of 2022, while Germany and France continued to experience lower production levels.

By 2023, a downturn began, particularly impacting Germany and Italy, which together accounted for a significant portion of Eurozone industrial production. In contrast, production remained stable in France and Spain. By 2024, industrial production in Germany was still 11.8% below its 2019 level, and Italy, France, and Spain were also showing shortfalls.

The decline since 2023 has been concentrated in specific sectors, with the automotive industry, machinery, electronics, fabricated metal products, and chemicals contributing to the downturn. Conversely, the pharmaceutical and food industries showed slight positive growth.

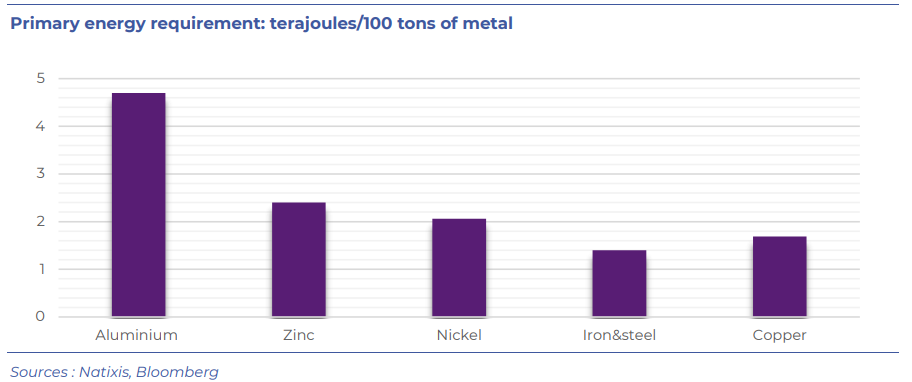

A Deeper Diver on the Aluminium Sector

Aluminum production is highly sensitive to energy prices, with electricity costs averaging 34.2% of total production expenses over the past decade, making it the most energy-intensive metal to produce. Following the onset of the Russia-Ukraine conflict, European energy prices surged, leading several EU producers to shut down their smelters. By 2022, the average energy share of cost in EU aluminum production rose to 38%, with Spain reaching 50%.

Although lower energy prices have allowed some producers in France to reopen their smelters, as of 2024, over half of the EU's production capacity remained offline. Despite a significant reduction in electricity prices from their peak, not all smelters can restart economically. The situation is complicated by the influx of Canadian aluminum into the EU market, as Canada has become uncompetitive in the U.S. due to tariffs.

For producers to restart, they require a stable long-term electricity price and sufficient profit margins. Restarting a smelter that has been shut down can take up to six months, prompting operators to be cautious about reopening. A potential peace agreement between Russia and Ukraine could further lower energy prices, improving margins and supporting the case for resuming production.

The decline since 2023 has been concentrated in specific sectors, with the automotive industry, machinery, electronics, fabricated metal products, and chemicals contributing to the downturn.

Several factors have contributed to the decline in German and Italian industrial production, particularly the surge in energy prices following the Russian invasion of Ukraine, which heavily impacted energy-intensive industries. The industrial composition in these countries is also more focused on sectors sensitive to investment cycles, such as automotive and machinery manufacturing.

The chemicals industry has seen a notable decline in production due to its high sensitivity to energy price fluctuations, with German production down 15% from pre-COVID levels. The automotive industry is facing challenges from rising energy costs and increased competition, particularly from China in the electric vehicle market. Since early 2024, Italy has experienced a significant drop in car production, with a 22.6% decline compared to previous years, while other countries also reported decreases, albeit to a lesser extent.

Reforming the European Electricity Market

The significant increase in electricity prices and operating costs has sparked discussions about the limitations of the current wholesale pricing system, which is largely based on fossil fuel prices through the merit order system. This model ranks energy sources by their marginal costs, leading to market prices determined by the last unit needed to meet demand. The 2022 crisis has raised concerns about the appropriateness of this system for ensuring cost competitiveness in European industries.

Debate has emerged over potential reforms to the European electricity market, with some advocating for a return to national pricing systems. However, this approach poses practical challenges, including the loss of a unified pricing mechanism and the reintroduction of regulated tariffs, which may conflict with European competition laws.

A prevailing approach within the EU emphasizes maintaining the current market organization for balancing purposes while adapting it to provide stable and competitive prices for energy-intensive industries.

In contrast, a prevailing approach within the EU emphasizes maintaining the current market structure while adapting it to provide stable and competitive prices for energy-intensive industries. This perspective has influenced recent proposals from the European Commission aimed at fostering Europe's reindustrialization and promoting a low-carbon electricity supply.

The New Market Design proposed in March 2023 seeks to decouple electricity prices from gas prices while preserving the merit order system for short-term pricing.

Financing Nuclear Newbuilds in France

France is emerging as a potential « testing ground » to finance new nuclear builds in a bid to maintain industrial competitiveness. It is seen as crucial for reindustrialization, especially after decades of declining manufacturing output.

Three key factors contribute to France’s positioning in this regard: 1. Historically, France's industrial competitiveness was significantly bolstered by an abundant and low-cost nuclear power supply, 2. The French government has clearly articulated its intention to enhance energy sovereignty and accelerate decarbonization through an ambitious plan to construct six, possibly fourteen, EPR2 reactors by 2050, and 3. The ongoing overhaul of the French electricity market.

In March, the French government outlined a financing strategy for the new nuclear builds, which includes a subsidized government loan covering at least 50% of construction costs, like the support received by the Czech nuclear program, and a two-way contract for difference (CfD) with a maximum remuneration of €100/MWh, aimed at stabilizing EDF's revenue after the construction phase.

The Draghi Report : A Systemic Approach to European Competitiveness from an Energy Perspective

The Draghi Report examines energy, gas, and electricity prices in relation to the competitiveness of the European economy, particularly for industrial activities.

The report builds on initiatives from the European Commission, such as the RepowerEU plan and a proposal for a New Market Design for the electricity sector, and offers additional recommendations. Key proposals include simplifying permitting processes, promoting power purchase agreements (PPAs), and encouraging self-generation.

Notably, the report advocates for maintaining existing nuclear energy supplies while expanding nuclear capacity and supporting carbon capture, utilization, and storage (CCUS) technologies to decarbonize industrial and energy assets. It also suggests several tools to support industrial demand, including: Counter Guarantees, Pooling Demand, and Legislative Action to allow Member States to introduce mechanisms where some electricity volumes can be sold at cost to energy-intensive industries

These measures aim to enhance the stability and competitiveness of European industrial production in the energy market.

France could also adopt corporate cooperative financing models, similar to the Exeltium scheme, which allows energy-intensive industries to secure long-term electricity supplies. This approach involves upfront payments from industrial customers to indirectly help power producers finance new nuclear projects while ensuring stable and competitive pricing.

Watch the Webinar Replay

[1] compared to 1990 levels