Deal Contingent : the Optimal Hedging for M&A Transactions

In light of lengthening M&A deal completion times and increased volatility in rates, currencies, and commodities, financial departments must secure the financial parameters of these pivotal transactions while retaining flexibility against the risk of non-completion. Deal contingent hedges are progressively emerging as a strategic tool to address this dual challenge.

This week in La Lettre du Trésorier, Paul Eterstein Global Head of FX & Rates Sales and David Sciolette, Global Head of Rates & FX for Corporates, SSA and Sponsors, contributed an opinion piece detailing its mechanics, its advantages in a turbulent context, highlighting the key role of treasurers in these transforming transactions.

David Sciolette

Paul Eterstein

Highly Volatile Markets

The monetary tightening cycle, spearheaded by major central banks over the past 18 months, coupled with an unstable geopolitical landscape, has driven significant volatility across financial markets. These developments profoundly alter corporate financing conditions and re-center risk management - particularly for interest rates - at the core of financial executives' concerns.

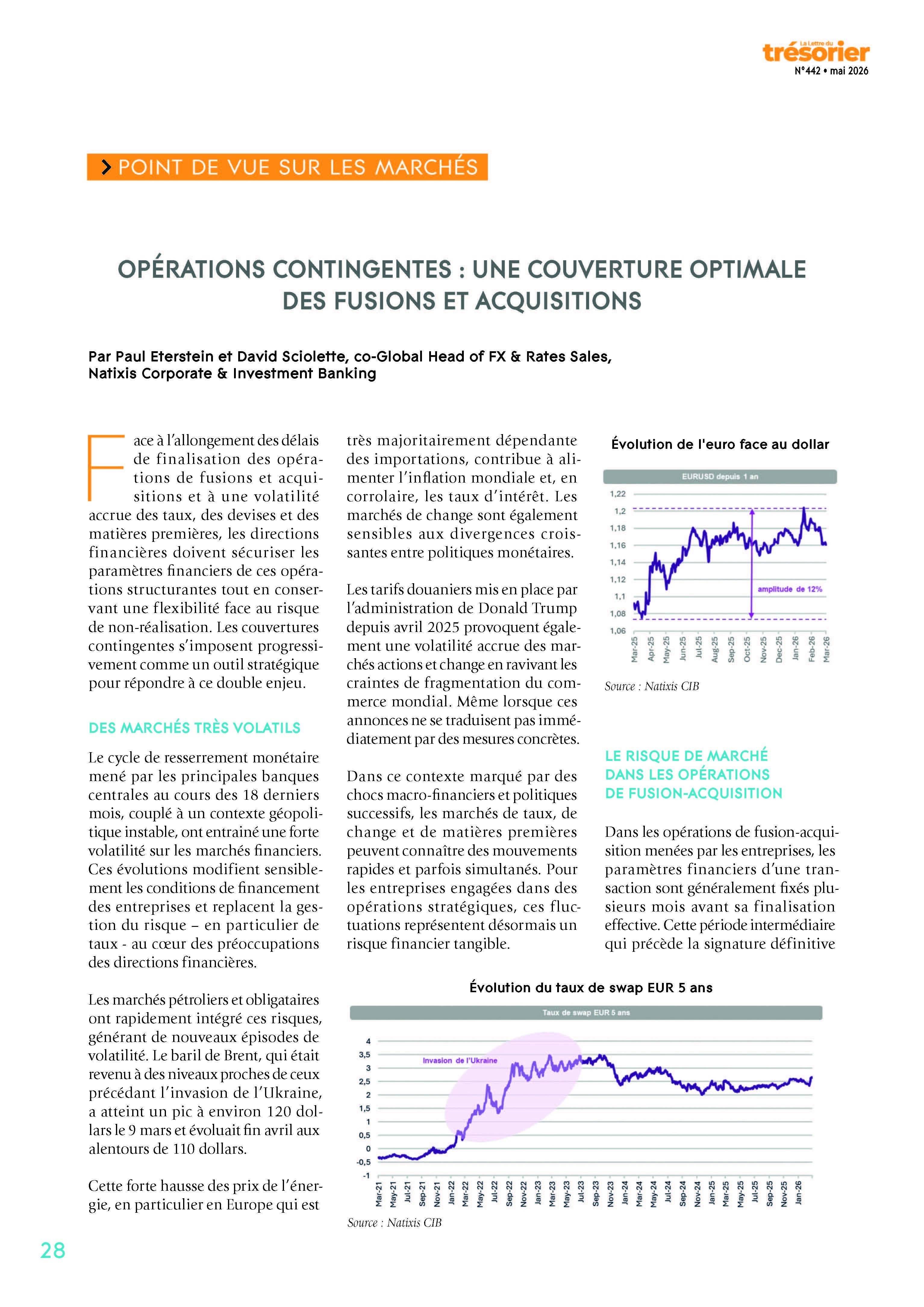

For instance, the 5-year EUR swap rate swung from negative territory to 3.4% within months following Russia's invasion of Ukraine in January 2022, and has since fluctuated between 2% and 3%. In recent weeks, escalating military tensions involving Iran have reignited anxieties regarding global energy supply stability, given the Strait of Hormuz's strategic role in international oil trade.

Oil and bond markets have rapidly priced-in these risks, triggering renewed bouts of volatility. The Brent crude barrel, which had returned to pre-Ukraine invasion levels, peaked around $120 on March 9th and is now trading near $110.

This sharp rise in energy prices, especially in Europe, heavily reliant on imports, contributes to global inflation and, consequently, to higher interest rates. Foreign exchange markets are also sensitive to growing divergences in monetary policies.

Tariff measures implemented by the Donald Trump administration since April 2025 are also creating heightened volatility in equity and currency markets by reviving fears of global trade fragmentation, even when such announcements do not immediately translate into concrete actions.

Within this context, marked by successive macro-financial and political shocks, rate, currency, and commodity markets can experience rapid and sometimes simultaneous movements. For companies engaged in strategic transactions, these fluctuations now represent a tangible financial risk.

In M&A, the challenge lies in securing transaction financials without introducing additional risk should the deal falter. Deal Contingent Hedges offer precisely this flexibility.

Paul Eterstein

Deal Contingent Hedges: Managing the Uncertain

In corporate M&A transactions, the financial parameters of a deal are typically set many months before its effective completion. This interim period, leading up to final signing, constitutes a phase of exposure to market fluctuations.

In the case of a cross-border transaction, currency fluctuations can also significantly alter the price paid by the acquirer. If the acquisition is debt-financed, a rise in interest rates between signing and completion can substantially increase financing costs. This risk is amplified as transaction timelines tend to lengthen.

Foreign investment controls, antitrust investigations, and sector-specific regulatory reviews have become more frequent and rigorous in numerous jurisdictions. Over the past three years, the M&A landscape has been characterized by unprecedented activism from competition authorities (notably the FTC in the US and the European Commission). Consequently, in 2024, the rate of blocked or abandoned deals in Europe reached 20%.

In certain instances, these processes can delay transaction completion by several months, or even longer. This period of uncertainty thus represents a potentially significant phase of exposure to market fluctuations.

For treasurers, this situation creates an evident dilemma: hedging too early exposes the company to the risk of unwinding the hedge should the transaction not materialize. Conversely, waiting until deal completion to hedge leaves the company vulnerable to unfavorable market movements.

We observe a growing use of these structures to simultaneously secure foreign exchange risk and transaction financing conditions. They provide visibility in a market environment that has become much more uncertain.

David Sciolette

Progressive Diversification of Covered Risks

Initially focused on covering foreign exchange risk, deal contingent hedges have progressively expanded to encompass other types of financial risks.

They are now employed to cover: interest rate risk, particularly when the acquirer plans to raise debt post-completion; commodity risk, when commodities are a key factor in the economics of an industrial project; and inflation indices, in certain long-term financing arrangements.

Early Involvement of Treasurers

The rise of these solutions is also accompanied by an evolution in the role of treasury teams within companies. Traditionally, treasurers might be involved relatively late in the acquisition negotiation process. Today, they are often engaged from the early stages of M&A transactions.

Their role involves not only analyzing potential financial exposures but also proposing hedging strategies tailored to the transaction's timeline and characteristics. In some transactions, hedging strategies are now implemented within hours or days of signing an acquisition agreement.

Specific Accounting Treatment

Beyond economic risk management, the implementation of hedges within M&A operations also raises significant accounting considerations.

Indeed, derivative instruments used to hedge interest rate or currency risks are typically accounted for at fair value, which can lead to fluctuations in financial statements even before the underlying transaction is completed. Without specific treatment, this situation can generate significant accounting volatility in the income statement.

However, international accounting standards, notably IFRS 9, permit the use of "hedge accounting," a framework designed to align the accounting recognition of gains and losses on derivatives with that of the hedged exposure.

Leading European statutory auditors now possess a thorough understanding of deal contingent derivative transactions and recognize their relevance.

In practice, implementing this treatment requires formal documentation of the hedging relationship, proof of its effectiveness, and regular ongoing monitoring.

These considerations must therefore be integrated from the outset of structuring the hedging strategy to ensure coherence between risk management, financial communication, and the presentation of financial statements.

In a volatile environment, several best practices emerge for managing market risk in M&A operations

- identify exposures early in the transaction process;

- analyze the transaction's sensitivities to rate, currency, or commodity variations upstream;

- integrate execution risk into the hedging strategy;

- consider the closing timeline and identify regulatory risks to be factored into the structuring of hedging instruments;

- combine traditional instruments with deal contingent solutions.

Classic instruments remain perfectly suited for certain exposures, while deal contingent hedges are particularly useful for conditional exposures.

Key Points of Focus for Treasurers

|

Key Principle |

Summary |

|

Triggering Event |

The transaction is subject to specific conditions (e.g., antitrust approval, successful closing of the acquisition/divestiture) to be valid. If not met, it will be voided. |

|

Main Goal |

Hedging against market risk (currency/interest rate/commodity etc.). |

|

Cost |

Included in the price if the transaction is activated. |

|

Flexibility |

Allows financial commitment only when required, optimizing costs compared to "full" options. It avoids paying for unnecessary protection. |

A Central Element

In an environment characterized by heightened financial market volatility and an increase in geopolitical and political uncertainties, market risk management has become a central element of M&A transactions.

Deal contingent hedges offer treasurers a particularly well-suited tool to secure a transaction's financial parameters while retaining the necessary flexibility in the face of uncertainty surrounding its completion.

Their progressive adoption reflects a broader transformation in the role of corporate treasury, which is now at the forefront of financially securing strategic operations in an increasingly uncertain economic climate.

Read Original in French